Sensitive financial data exposure

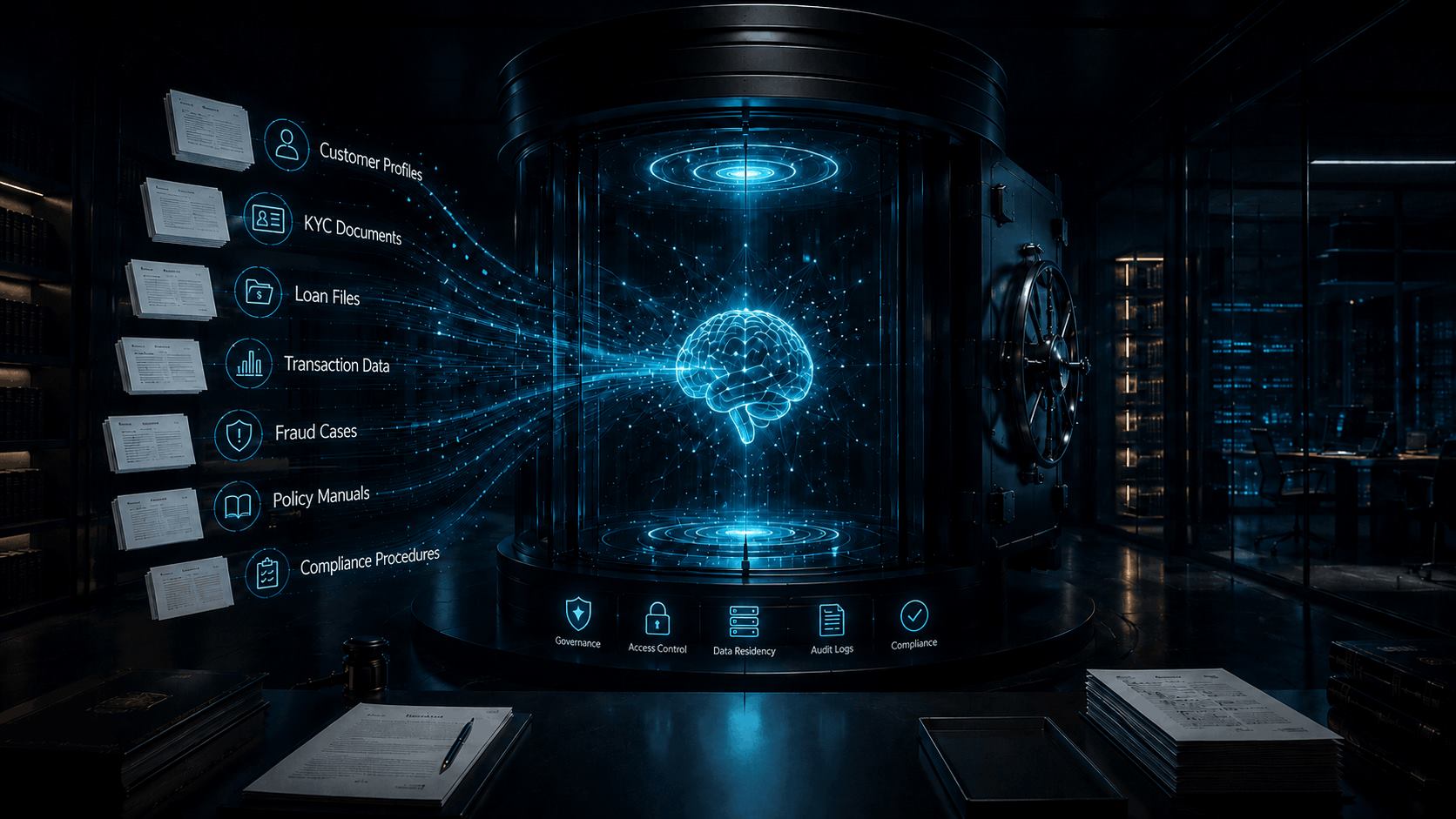

Customer records, transaction data, credit information, financial statements, investigation records, and business data need controlled handling.

Banking and financial services

Build banking intelligence your institution can own.

Banks, credit unions, lenders, fintech companies, payment providers, wealth managers, and financial institutions are adopting AI quickly. The durable advantage comes from converting approved policies, risk procedures, customer interactions, investigation history, lending guidelines, compliance knowledge, and operational decisions into private AI intelligence.

Private AI for banking keeps financial data, prompts, retrieval, outputs, access permissions, and audit records inside controlled infrastructure.

Banking AI agents support workflows across KYC, AML, lending, fraud, customer service, payment operations, and compliance.

Task-specific SLMs are useful where work is language-heavy, document-intensive, high-volume, and governed by institution-specific rules.

The challenge

Financial institutions are experimenting with generative AI, copilots, conversational AI, and autonomous agents. As adoption expands, the key question becomes practical: can the institution secure it, explain it, govern it, control its cost, and integrate it into regulated banking workflows?

Customer records, transaction data, credit information, financial statements, investigation records, and business data need controlled handling.

Customer histories, lending files, investigation cases, compliance policies, and regulatory documents can create repeated large-context processing.

Data often sits across core banking, loan origination, CRM, fraud tools, payment systems, compliance platforms, document repositories, and warehouses.

Documents, validation, policy checks, reconciliation, investigations, approvals, and customer follow-ups often escape simple automation.

Banking AI needs evidence, source traceability, controlled actions, approval thresholds, and complete audit records.

The SLM advantage

Banking does not require one large model to perform every task. The strongest architecture combines predictive models for scoring, deterministic rules for policy enforcement, task-specific SLMs for language and document workflows, private RAG for institutional knowledge, AI agents for orchestration, and human review for material decisions.

Defined tasks: customer-intent classification, KYC document review, compliance alert triage, policy matching, case summarization, and exception routing.

Approved knowledge: product policies, KYC procedures, AML guidelines, lending rules, compliance manuals, service scripts, and historical case outcomes.

Deployment control: on-premises, private cloud, controlled VPC, dedicated GPU, region-specific hosting, or hybrid AI architecture.

Detailed use cases

The strongest opportunities are language-heavy, document-intensive, high-volume, and governed by institution-specific rules. The aim is to automate preparation, investigation, evidence gathering, routing, and repetitive decision support while preserving accountable human judgment.

01

Coordinate onboarding across documents, customer channels, screening systems, and internal reviewers.

02

Collect evidence, summarize findings, compare cases with approved procedures, and prepare investigation records.

03

Structure applications, income documents, statements, collateral details, credit files, and supporting evidence for review.

04

Accelerate the investigation and resolution workflow around fraud engines without replacing approved risk-scoring models.

05

Answer approved questions and complete controlled actions across digital, branch, and contact-center channels.

06

Retrieve institution-approved information with source traceability and role-based access for internal teams.

07

Support the information and preparation layer while qualified professionals retain approval responsibility.

08

Gather data across systems, classify exceptions, and prepare payment cases for resolution.

09

Compare documents, extract obligations, and flag discrepancies for trained reviewers.

10-11

Private AI can organize approved product knowledge, customer history, research, and follow-up drafts for advisors, while collections teams can use controlled language, approved options, vulnerability escalation, and human handoff for sensitive customer interactions.

Client-meeting preparation

Approved-product retrieval

Promise-to-pay capture

Vulnerability escalation

Operations layer

A useful banking AI system should help teams move cases through onboarding, verification, risk review, approval workflows, service requests, fraud investigation, and compliance preparation with clear escalation and human review.

Onboarding teams get faster KYC intake, document extraction, and missing-information routing.

Financial crime teams get cleaner alert summaries, evidence packs, and case narratives.

Lending teams get structured document review, policy comparison, and underwriter-ready files.

Service teams get approved response support, controlled actions, and human handoff.

How we help

Sovereign SLM Labs helps financial institutions move from disconnected AI pilots to governed, institution-owned AI capability.

We identify where private AI can create value across customer service, lending, compliance, financial crime, payments, operations, and employee productivity.

We design agents around defined workflows, permissions, business rules, validation steps, and approval thresholds.

We select, fine-tune, and adapt Small Language Models according to the workflow, accuracy requirements, infrastructure, and risk profile.

We route each task to the right model or system based on sensitivity, complexity, risk, cost, and accountability.

We help deploy banking AI in controlled infrastructure aligned with privacy, data residency, latency, risk, and governance requirements.

We build secure retrieval systems over institution-approved information with source traceability and role-based access.

We connect private AI with the systems banking teams already use so agents support real workflows rather than isolated demos.

We design controls around access, validation, source traceability, action permissions, monitoring, drift detection, fairness testing, and change management.

Architecture

A strong banking AI architecture should route work according to data sensitivity, complexity, risk, cost, and accuracy requirements. It should combine SLMs, private RAG, predictive models, deterministic rules, controlled larger models, workflow actions, audit logging, and human escalation.

Customer-intent classification can go to a small private model.

Document extraction can go to a task-specific banking SLM.

Policy questions can use private RAG over approved sources.

Fraud and credit scoring should use approved predictive models and rules, with SLMs supporting explanations and case preparation.

Governance note

Private AI can support KYC, AML, lending, fraud, customer service, and compliance workflows, but the operating model matters. Material decisions should follow approved institutional policies, models, procedures, reviews, disclosures, and accountability controls. A useful system keeps evidence, source links, action permissions, confidence thresholds, audit logs, and escalation rules visible from the start.

Least-privilege access and data-residency controls

Source traceability and output validation

Human approval and exception escalation

Model versioning, monitoring, and change control

Related reading

These pages expand the architecture patterns behind local deployment, model routing, private RAG, and cost-aware SLM strategy.

Workshop

Explore how Sovereign SLM Labs can help your institution build secure, task-specific AI around banking and financial-services workflows.

Identify one high-value banking workflow suitable for private SLMs.

Assess data, infrastructure, governance, and integration requirements.

Build a practical private AI implementation roadmap.

FAQ

Private AI for banking refers to AI systems deployed within controlled infrastructure where financial data, prompts, retrieval pipelines, outputs, access permissions, and audit records remain governed by the institution.

Banking AI agents are software systems that interpret requests, retrieve approved information, perform defined workflow actions, interact with authorized banking systems, and escalate exceptions under institutional guardrails.

A banking SLM is a smaller, specialized language model trained or adapted for a defined task such as KYC extraction, alert classification, policy matching, case summarization, customer-intent routing, or document review.

An SLM is narrower, easier to optimize, and potentially more predictable for repetitive workflows. A broad LLM offers wider reasoning capability but may require more infrastructure, cost, and governance.

Not usually. Fraud and credit scoring are generally better handled by approved predictive models, statistical systems, and rules engines. SLMs are more suitable for document processing, case analysis, explanations, customer interaction, and workflow orchestration.

Yes. Private AI can assist with document extraction, alert review, adverse-media analysis, customer-profile summarization, evidence collection, narrative drafting, and analyst routing while keeping accountable review and approval controls in place.

AI agents can prepare underwriting cases, extract data, compare applications with policy, and identify exceptions. Final lending decisions should follow the institution's approved models, policies, controls, and human-approval requirements.

Yes. Agents can connect with core banking, CRM, lending, payments, fraud, compliance, case-management, and document systems through authorized APIs and controlled integrations.

Yes. Depending on model size and infrastructure, private SLMs, banking AI agents, and RAG systems can run on-premises, in private cloud, within a controlled VPC, or through a hybrid architecture.

Private RAG retrieves relevant information from institution-approved policies, procedures, cases, product materials, and knowledge sources, then provides evidence-linked context to the model without exposing the full knowledge repository externally.